Chart courtesy of Memoori Research

According to research company Memoori, cyber security consistently ranks as one of the top 3 concerns worrying organisations that are considering investment in IoT or digital transformation projects.

The analysts found that spending on cyber security has surged in recent years, driven by major trends including the rise in ransomware attacks, a series of high-profile breaches and the massive security challenges posed by the transition to more remote work and the accelerated push for digital transformation.

Memoori’s new report estimates that in 2021, global revenues for smart building cyber security hardware, software and services reached $4.33Bn, and the company expects the market to achieve a CAGR of 12.2% over the next five years, rising to a combined value of $8.65Bn by 2027. This 2nd edition of research into the market for cyber security in smart commercial buildings focuses on market sizing and opportunities, and it provides a fresh assessment based on the latest available data and in-depth market analysis. And it also includes a spreadsheet containing the data from the report and a graphics pack with high-resolution charts.

The research suggests that end users and vendors should, as for the implementation of any new technology, consider cyber security needs throughout the design and build process, embedding the right security/privacy controls and risk mitigation solutions at each stage of development. Meeting the latest cyber security standards and getting IoT products officially certified can provide a clear competitive advantage for vendors when tendering for new business.

In terms of competitive landscape, Memoori analysts say that the market has attracted vendors with a range of different backgrounds and specialisations. As well as being serviced by a number of niche, smart buildings-focused firms, the vendor landscape now includes a combination of players with backgrounds in building, ICT hardware/software, consulting, IT-focused cyber security software and service, OT/Industrial focused cyber security software & services and IoT device security.

The market sizing and forecasts presented in the report are based on a custom market model and iterative research methodology. This new research builds on decades of experience in the evaluation of a wide variety of smart building-related markets with a particular focus on tracking and evaluating the performance of a variety of technology markets and their impact on commercial buildings.

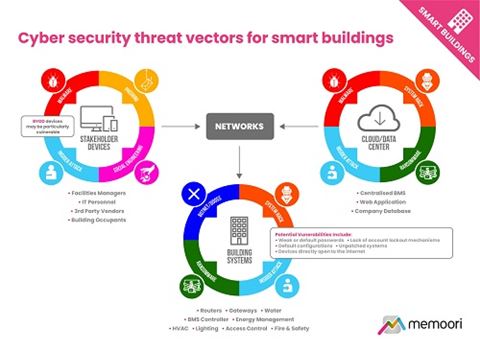

The market challenges are varied, but the Memoori study suggests that arguably the most challenging aspect of effectively managing cyber risk for smart buildings is the major differences between historical approaches to systems design and operations, and divergent priorities between Information Technology (IT) systems and Operational Technology (OT) systems.

Rising levels of cyber risk posed by IoT devices and connected smart building systems is having a significant adverse effect on building owners’ ability to effectively insure their assets, with some industry observers even going so far as to state that “the lack of effective cyber cover is rapidly becoming a leading barrier to smart building adoption moving forward”.

There is also a concern that a large proportion of smart building owners and operators could be totally unaware that they have no legitimate insurance cover for their smart building systems and would be fully liable for all associated costs in the event of a cyber breach – truly a concerning state of affairs.

The positive take-home is that the analysis indicates the market will prove resilient despite a challenging global economic environment, as combined forces including the ever-increasing levels of digitisation of built environment assets, the rising incidence of cyber-attacks, rising cost implications of successful data breaches, and increasingly stringent cyber security & privacy related legislation continue to spur spending growth.

Source: SECURITY WORLD MARKET